How to Calculate IRR: The Definitive Guide for Multifamily Real Estate Investors

- Justin Brennan

- Mar 1

- 12 min read

Stop letting complex spreadsheets kill your deal flow. In the high-stakes game of Multifamily real estate, speed and accuracy are everything. The difference between a good deal and a great one-or a catastrophic one-often comes down to one critical metric. Hesitate, and you lose the deal. Calculate incorrectly, and you lose your capital. This is where mastering how to calculate IRR becomes your ultimate competitive advantage. It’s the metric that separates the amateurs from the operators who are truly Scaling Up.

Forget the financial jargon and the fear of bad math. This definitive guide is your blueprint to dominate deal analysis. We will demystify the entire process, giving you the tools to underwrite 100+ unit assets with institutional-grade precision, articulate returns to your investors with unshakeable confidence, and accelerate your path to generating massive Passive Wealth. It’s time to unlock the Multifamily Mindset and start making smarter, faster, and more profitable decisions.

Key Takeaways

Master IRR, the gold-standard metric private equity uses to instantly compare and dominate multifamily opportunities.

Distinguish between Levered and Unlevered IRR to unlock the true return on your equity and understand the power of your capital stack.

Execute a step-by-step framework on how to calculate IRR, transforming your underwriting from guesswork to a precision instrument for deal analysis.

Identify the most common underwriting traps-aggressive exit caps and fantasy rent growth-to instantly spot fake IRR projections and protect your capital.

Table of Contents What is IRR and Why Does it Rule the Multifamily World? The IRR Formula: Decoding the Mechanics of Your Deal Unlevered vs. Levered IRR: The Power of the Capital Stack How to Calculate IRR: Tools and Step-by-Step Execution Underwriting for Success: How to Spot 'Fake' IRR Projections

What is IRR and Why Does it Rule the Multifamily World?

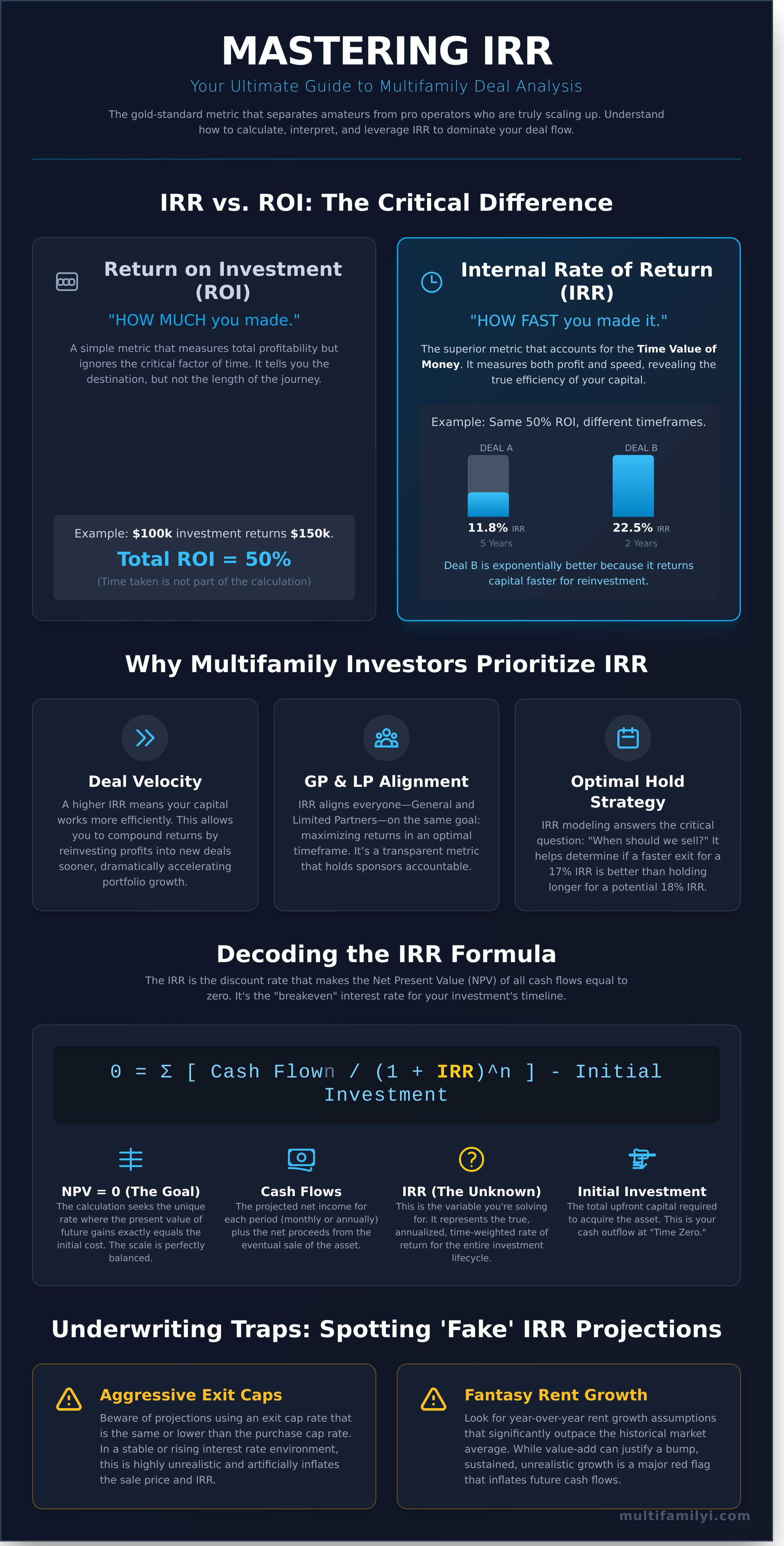

In the high-stakes world of multifamily real estate, one metric reigns supreme. Before you even think about how to calculate IRR for that prime La Jolla deal, you must understand why it's the metric that separates the pros from the pack. Forget simple returns; we’re playing a different game. The Internal Rate of Return (IRR) is the annualized effective compounded rate of return that makes an investment's future cash flows equal to the initial investment. In simpler terms, it's the true measure of a deal's performance over time.

This isn't your basic Cash-on-Cash return, which only measures a single year's cash flow. IRR accounts for the Time Value of Money (TVM), a core principle stating that a dollar today is worth more than a dollar tomorrow. IRR understands that a profitable exit in year three is vastly more powerful than the same profit in year seven because you can redeploy that capital to accelerate your wealth creation. It's the gold standard in syndications and private equity because it measures both profit and speed.

The Difference Between ROI and IRR

Think of it like this: ROI tells you how much you made; IRR tells you how fast you made it. Imagine you invest $100,000 and get $150,000 back in five years. Your total ROI is 50%. Not bad. But what if another deal delivered that same 50% ROI in just two years? The second deal’s IRR would be exponentially higher. A 15% IRR on a 3-year deal is far more valuable than a 50% total ROI on a 10-year deal because it puts capital back in your hands faster, ready for the next acquisition.

Why Multifamily Investors Prioritize IRR

For serious operators looking to scale, IRR is the ultimate key performance indicator. It’s the engine of portfolio growth and the universal language between General Partners (GPs) and Limited Partners (LPs). Here’s why it’s non-negotiable:

Deal Velocity: A higher IRR means your capital is working more efficiently. This allows you to compound returns by reinvesting profits into new deals sooner, dramatically accelerating the growth of your portfolio.

GP & LP Alignment: IRR aligns everyone on the same goal: maximizing returns in an optimal timeframe. It’s a transparent metric that holds the deal sponsor accountable for the entire lifecycle of the asset, from acquisition to exit.

Optimal Hold Strategy: Understanding how to calculate IRR allows you to model exit scenarios. For a 100-unit complex, it answers the critical question: do we sell in year 3 for a 17% IRR or hold until year 5 for a potential 18% IRR? Often, the faster exit unlocks greater long-term wealth.

The IRR Formula: Decoding the Mechanics of Your Deal

To dominate in multifamily investing, you must master the metrics that define a winning deal. The Internal Rate of Return (IRR) is chief among them. At its core, the IRR is the specific discount rate that forces the Net Present Value (NPV) of all future cash flows from an investment to equal zero. This is the key to understanding how to calculate IRR and what it truly represents: the annualized, time-weighted return of your capital.

The formula looks complex, but the concept is straightforward:

0 = NPV = Σ [Cash Flow / (1 + IRR)^n] - Initial Investment

Let's break down the variables that drive your deal's performance:

Initial Outlay: This is your upfront capital injection-the total cash required to acquire the asset.

Cash Flows: These are the projected net cash flows for each period of the hold, including rental income and the final proceeds from the sale.

The Discount Rate (IRR): This is the unknown you're solving for. It's the unique interest rate that makes the present value of your future cash flows exactly equal to your initial investment.

Manually solving for IRR is a grueling trial-and-error process of plugging in different rates until the NPV equation balances to zero. For a technical breakdown of this process, Investopedia's guide to IRR offers a detailed look. However, elite operators don't waste time on manual calculations; we leverage the power of Excel or sophisticated underwriting software to get an instant, precise answer. Your focus should be on the inputs, not the arithmetic.

Understanding Net Present Value (NPV)

Think of NPV as the engine driving your IRR calculation. It measures the current value of all future cash flows, discounted back to today to account for the time value of money. There's a critical inverse relationship here: as the discount rate you apply goes up, the NPV of your deal goes down. In essence, NPV represents the total 'profit' of the deal, expressed in today’s dollars.

The Role of the Discount Rate

Your chosen discount rate is a reflection of risk and opportunity cost. For a high-potential La Jolla deal, you might demand a higher return than for a stabilized asset in a secondary market. Sophisticated multifamily investors often use the Weighted Average Cost of Capital (WACC) to create a precise discount rate. Remember, inflation is a silent killer of returns; a high-inflation environment demands a higher required return just to break even.

This required rate of return is your Hurdle Rate. In a multifamily syndication, the hurdle rate is the minimum return that must be achieved before the general partner (the sponsor) earns their promoted interest. It’s the performance benchmark that unlocks the next tier in the equity waterfall, aligning the sponsor's success directly with the passive investors' returns.

Unlevered vs. Levered IRR: The Power of the Capital Stack

To truly master how to calculate IRR, you must understand the critical difference between unlevered and levered returns. One measures the raw potential of the asset; the other measures the magnified return on your actual cash investment. This distinction is where elite operators unlock massive wealth.

Unlevered IRR: This is the pure, unadulterated return of the La Jolla property itself. It assumes you paid all cash, with zero debt. Think of it as the asset's intrinsic performance.

Levered IRR: This is the return on your equity-the cash you and your investors put into the deal. It accounts for all debt service (principal and interest payments) and reveals the true power of your capital stack.

When the property's unlevered return is higher than your cost of debt, you achieve 'Positive Leverage.' This is the secret sauce. By using the bank's money, you amplify your returns, turning a solid deal into an absolute home run. But be warned: if interest rates spike and your cost of debt exceeds the property's return, you'll face 'Negative Leverage' that can crush your IRR and your capital.

Calculating Returns with Debt

Let's make this real. Imagine your La Jolla deal has a 7% Unlevered IRR. Solid, but not life-changing. Now, you secure intelligent debt at 75% LTV. Suddenly, that 7% blossoms into a 15% Levered IRR. Your equity is working twice as hard. Add an interest-only (IO) period, and you supercharge early-year cash flow, further boosting the IRR. This is why lenders fixate on the Unlevered IRR-it shows them the underlying asset can perform, even if your specific financing structure changes.

Risk-Adjusted Returns

A sky-high Levered IRR isn't always the goal. Aggressive debt might pump up the number, but it also dramatically increases your risk. As Forbes notes, a high IRR can be a misleading statistic if it ignores the risk profile. The art is in balancing the capital stack to protect your downside while chasing that epic return. You need to model different scenarios instantly. Use a tool like the Multifamily Analyzer to toggle LTV, interest rates, and amortization, so you can engineer a capital structure that delivers both performance and peace of mind.

How to Calculate IRR: Tools and Step-by-Step Execution

Theory is for the classroom. In the high-stakes world of multifamily investing, execution is everything. Knowing how to calculate IRR is the critical skill that separates ambitious investors from institutional-grade operators. This is where you translate your underwriting into a single, powerful metric that drives decisions.

Follow this battle-tested, four-step process to nail your IRR calculation every time.

Step 1: Determine the Initial Investment. This is your total cash outflow at Year 0. Sum the acquisition price, all closing costs, and any immediate capital expenditures planned for renovations. This number is your initial negative cash flow.

Step 2: Project Annual Net Cash Flows. Forecast your Net Operating Income (NOI) for each year of your planned hold period. After subtracting your annual debt service, you are left with the property's cash flow for each year.

Step 3: Estimate the Net Sales Proceeds. Project the property’s future sale price using a conservative exit cap rate. From this exit value, subtract selling costs and the remaining loan balance to find your net profit on sale. Add this lump sum to the final year's cash flow.

Step 4: Run the Calculation. With your complete cash flow stream mapped out-from the initial investment to the final exit-it's time to use a financial tool to find the discount rate that makes the Net Present Value (NPV) of all cash flows equal to zero.

The Excel Method for Rapid Analysis

For a quick back-of-the-napkin analysis, Excel is your go-to. Set up a simple column with your timeline (Year 0, Year 1, etc.) and an adjacent column with the corresponding cash flows. The single most common mistake is forgetting the negative sign for your initial investment in Year 0. Your formula is simply =IRR(values). For more precision, especially with irregular cash flow timing, use the =XIRR(values, dates) function to unlock a more accurate, real-world return profile.

Professional Deal Analyzers vs. Manual Spreadsheets

Manual spreadsheets are a starting point, but they fail when deals get serious. Once you introduce complex structures like investor waterfalls or sponsor promotes, a simple IRR formula becomes useless. This is the ceiling that limits your ability to scale. To play at an elite level, you need professional-grade tools. Our Multifamily Analyzer is engineered to handle this complexity effortlessly, allowing 'One-Click' sensitivity analysis to stress-test your returns. It standardizes your underwriting, ensuring you present deals to brokers and partners with institutional credibility. Stop building formulas and start building your empire.

Underwriting for Success: How to Spot 'Fake' IRR Projections

You’ve learned the mechanics, but knowing how to calculate IRR is only half the battle. The real money is made by spotting fantasy pro-formas before you invest a single dollar. Amateurs get mesmerized by a big number; pros dismantle the assumptions behind it.

The number one way IRR is manipulated is through an overly aggressive Exit Cap Rate. A sponsor might buy a La Jolla property at a 5% cap rate but project selling it at a 4% cap in five years. This single assumption can inflate a mediocre deal into a home run on paper. It’s a bet on market perfection, not a sound investment strategy.

Watch these two critical weak points in any deal package:

Fantasy Rent Growth: Are they projecting 8% annual rent growth in a market that has historically averaged 3%? Demand real-world data, not hockey-stick projections that ignore economic cycles.

Terminal Value Dependency: If over 80% of your projected IRR comes from the Terminal Value (the sale), you’re not investing in cash flow-you’re gambling on a massive payout at the exit. This is a fragile foundation for building real wealth.

Sensitivity Analysis: Stress-Testing Your IRR

This is how you separate bulletproof deals from brittle ones. Ask the tough questions. What happens to the IRR if the exit cap rate expands by 50 or 75 basis points? Run a worst-case scenario where occupancy drops 10% for a year. Does the deal still work, or does it collapse? This is where understanding the nuances of how to calculate IRR truly pays off.

A key part of this stress-testing is staying informed about the broader economic and policy trends that can impact your assumptions. For human-centred journalism covering the intersection of business, policy, and identity in key global markets, you can learn more.

'A robust IRR survives a bad year; a fragile IRR requires a perfect exit.'

The Multifamily Intelligence Advantage

You don't have to underwrite in a vacuum. In The Network, you’re surrounded by operators and investors closing deals in markets like La Jolla right now. Our community provides the ground-truth data you need to pressure-test any sponsor's claims, turning their pro-forma into your proven financial model.

Stay ahead of market shifts with our newsletter, which tracks the cap rate trends that directly impact your exit strategy and overall returns. Stop guessing and start knowing. Ready to dominate? Join our 5-Day Multifamily Challenge and start analyzing deals today.

Master the Metric, Master the Deal

You now have the blueprint. You understand that IRR isn’t just a number-it’s the ultimate performance metric that separates amateur investors from professional operators in the multifamily world. You know the critical difference between unlevered and levered returns and, most importantly, you can now spot a deal built on fantasy projections. Mastering how to calculate IRR is your first, non-negotiable step toward underwriting with absolute confidence and building real, passive wealth.

But knowledge without execution is just theory. It's time to accelerate your growth. Stop analyzing deals in a vacuum and start building your empire with a proven system. Scale your portfolio with the Personal Mentorship Program and gain an unfair advantage. You'll get our proprietary Multifamily Analyzer software, direct feedback on your deal structures from Charles Dobens, and daily insights from 'The Multifamily Attorney' network.

The deals are out there. Go get them.

Frequently Asked Questions

Is a 20% IRR good for a multifamily investment?

A 20% IRR is an exceptional target that signals a highly profitable deal. For sophisticated investors in our network, this is the benchmark for a successful stabilized asset. While value-add projects often aim higher to compensate for increased risk, achieving a 20% IRR demonstrates you've dominated the underwriting and execution phases. It's a powerful indicator of your ability to generate significant passive wealth and scale your portfolio effectively. This is the level where true financial freedom is built.

What is the difference between IRR and Equity Multiple?

Think of it this way: IRR measures how fast your money grows, while Equity Multiple measures how much it grows. IRR is a time-sensitive metric that heavily weights early cash flows, making it critical for comparing deals with different timelines. The Equity Multiple provides a simple, powerful snapshot of your total cash-on-cash return over the life of the deal. Elite investors use both metrics to get a complete picture and make decisive, winning investment choices.

Can IRR be negative?

Absolutely, and it's a red flag you must avoid. A negative IRR means the investment lost money, failing to even return your initial capital. It signals a fundamental flaw in the deal's underwriting, operations, or exit strategy. This is precisely why rigorous analysis and leveraging an expert network are non-negotiable. Your goal is to accelerate wealth, not destroy it. A negative IRR is a clear sign that the deal's performance fell drastically short of its pro forma projections.

How does the hold period affect the IRR calculation?

The hold period is a massive lever in your IRR calculation. Because IRR prioritizes the time value of money, receiving your profits sooner dramatically boosts the final number. A shorter hold period with the same total profit will always yield a higher IRR than a longer one. This is why a quick, successful execution on a value-add business plan is so powerful-it compresses the timeline and accelerates your returns, unlocking your capital to reinvest and scale faster.

What is a 'Hurdle Rate' in real estate syndication?

A hurdle rate is the minimum return that limited partners (LPs) must receive before the general partner (GP) can collect their performance fee, or 'promote.' It's a critical mechanism that aligns interests and ensures the deal sponsor is laser-focused on delivering results. If the deal's IRR doesn't 'clear the hurdle'-typically set between 7-10%-the sponsor doesn't get their full share of the profits. It’s a key protection for passive investors in the deal.

Why do investors prefer IRR over ROI for apartment buildings?

Top-tier investors favor IRR because it tells the whole story. While ROI gives you a simple, static percentage, it ignores a critical factor: time. Multifamily deals involve multiple cash flows over many years-distributions, refinancing events, and the final sale. IRR accounts for the timing of every single dollar, providing a far more accurate and dynamic measure of a deal's true performance. It’s the professional’s metric for sophisticated, time-sensitive assets like apartment buildings, and the same principles apply to other high-value niche markets, such as those found on platforms like Colorado Horse Property.

How do I calculate IRR if I have irregular cash flows?

Irregular cash flows are the norm in multifamily investing, and IRR is the perfect tool to handle them. The process of how to calculate IRR with varying cash flows is best handled with a spreadsheet. Simply list all cash outflows (your initial investment) as negative numbers and all inflows (distributions, sale proceeds) as positive numbers by date. Then, use the XIRR function in Excel or Google Sheets. This function is specifically designed to calculate the IRR for a schedule of cash flows that is not necessarily periodic.

What is a 'good' IRR for a value-add multifamily project in 2026?

For a value-add multifamily project in 2026, sophisticated investors will be targeting a project-level IRR in the 16% to 22% range. This accounts for the higher risk and execution demands of a repositioning strategy. The exact target will depend on factors like leverage, the submarket's strength-like we see in prime locations such as La Jolla-and prevailing interest rates. Anything below this range may not provide enough compensation for the risk, while anything above it represents a home-run deal.

Comments