Mastering the Capital Stack: The Investor’s Blueprint for Funding Apartment Deals

- Justin Brennan

- Mar 16

- 15 min read

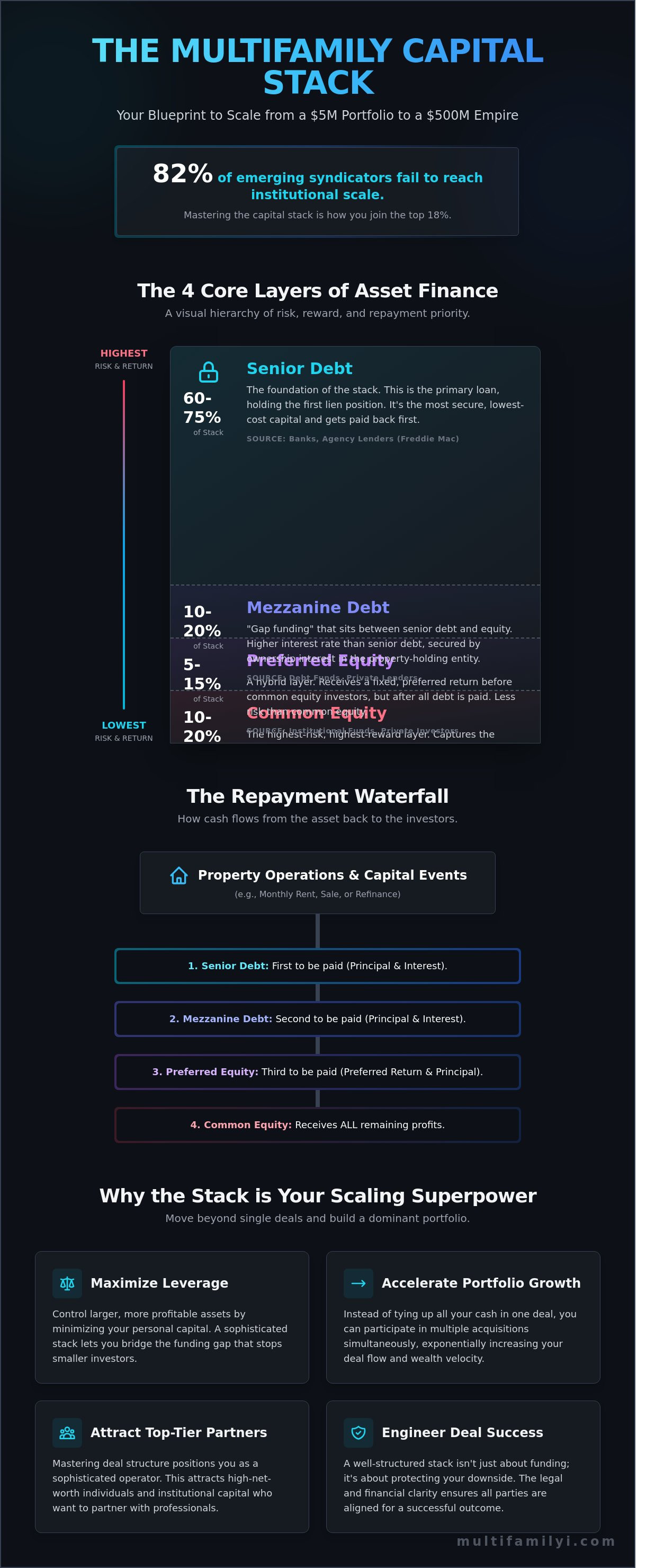

The difference between a $5 million portfolio and a $500 million empire isn't the size of the investor's bank account; it's the sophistication of their capital stack. You've likely felt the sting of watching a prime 150-unit asset slip away because you couldn't bridge a $750,000 equity gap. It's a frustrating ceiling that prevents 82% of emerging syndicators from ever reaching institutional scale. You recognize that smart leverage is the engine of wealth velocity, but the complexity of mezzanine layers or the fear of losing deal control often forces you to pass on life-changing opportunities.

It's time to stop playing defense and start engineering your funding for maximum impact. This blueprint will unlock the exact frameworks used by high-performance firms to layer senior debt and preferred equity into a dominant acquisition strategy. You'll learn to master the repayment waterfall with confidence and position yourself as a master deal-maker who attracts top-tier partners. We're providing the technical clarity you need to close bigger deals and accelerate your journey toward total passive wealth through the power of The Network.

Key Takeaways

Master the capital stack to identify exactly where your money sits and how to command the highest returns on every multifamily deal.

Decode the four core layers of asset finance to optimize your leverage and protect your downside in any market cycle.

Demystify the repayment waterfall to ensure you clearly understand the flow of cash from operations to high-stakes capital events.

Strategically engineer your financing structure to minimize your personal capital contribution and accelerate your portfolio growth.

Bridge the gap between technical deal-making and the Multifamily Lifestyle to unlock true passive wealth and total professional mastery.

Table of Contents What is the Capital Stack in Real Estate? Your Blueprint for Scaling Breaking Down the 4 Core Layers of a Multifamily Deal Repayment Priority: Understanding the Waterfall and Risk Strategic Structuring: How to Optimize Your Stack for Maximum Leverage Mastering the Stack: From Theory to High-Stake Deal Execution

What is the Capital Stack in Real Estate? Your Blueprint for Scaling

Multifamily investing isn't a hobby; it's a high-stakes game of financial engineering. In the competitive La Jolla market, where median sales prices for residential assets reached $2.7 million in late 2023, mastering the capital stack is your only way to play. Think of the stack as the total sum of every dollar invested in an asset. It represents the foundation of your deal. For sophisticated apartment investors, this is the line of scrimmage. If you don't understand the positioning of your capital, you aren't investing; you're gambling.

The stack provides a visual and legal representation of who owns what and who gets paid when. It functions as a roadmap for risk and reward. At the bottom, you find stability and lower returns. As you climb toward the top, the risk intensifies, but so does the potential for explosive growth. This structure is modeled after the broader corporate capital structure that dictates how firms finance their operations through different sources. In real estate, mastering this hierarchy allows you to unlock Passive Wealth and transition from a practitioner to a market leader. It's the ultimate tool for total lifestyle freedom.

The Hierarchy of Funding

Seniority is the heartbeat of the stack. It dictates the order of operations for every dollar the property generates. In the world of multifamily, your position in the stack determines your fate when the cash flows. The hierarchy is rigid, ensuring that those with the most security receive their payments first, while those at the top wait for the "upside" after all obligations are met.

Senior Debt: This is usually a bank or agency loan. It sits at the bottom, holds the first lien position, and typically covers 60% to 75% of the total project cost.

Mezzanine Debt: This layer sits above senior debt. It's often secured by the equity interests of the borrowing entity rather than the property itself.

Preferred Equity: This is a "hybrid" layer. Investors here get paid before the common equity holders but after the debt service is covered.

Common Equity: This is the top of the stack. These investors take the most risk but capture the majority of the profit once the asset hits its performance targets.

Why One Layer is Never Enough

Relying solely on senior debt is a strategy for the stagnant. Most institutional lenders in 2024 won't provide more than 65% of the capital needed for a value-add acquisition in high-demand areas like San Diego County. This creates a massive void known as "gap funding." Sophisticated stacks solve this problem by layering different types of capital to cover 100% of the acquisition and renovation costs.

Scaling up requires more than just a bank balance; it requires a network. When you have a deep bench of partners and co-investors, you can fill these layers quickly to maintain consistent deal flow. By using mezzanine or preferred equity, you reduce the amount of your own cash tied up in a single deal. This allows you to dominate multiple assets simultaneously. This strategy is how you accelerate your journey to professional mastery. You don't just buy a building; you build a financial engine that fuels your lifestyle while The Network handles the heavy lifting.

Breaking Down the 4 Core Layers of a Multifamily Deal

Mastering the capital stack separates the hobbyists from the heavy hitters in La Jolla's competitive market. You're not just looking at numbers on a spreadsheet; you're looking at the hierarchy of payment and the engine of your ROI. To dominate this space, you must understand exactly how these four layers interact to fuel your deal flow and protect your principal. Every dollar invested sits in a specific spot that determines when you get paid and how much risk you're carrying.

The Debt Layers: Senior vs. Mezzanine

Senior debt forms the bedrock of every serious multifamily acquisition. In the current 2024 lending environment, expect this layer to cover 65% to 75% of the total project cost. Institutional lenders like Wells Fargo or agencies like Freddie Mac provide this low-cost foundation. They demand the first lien position, which means they're the first to be made whole if a deal goes south. This security is why senior debt offers the lowest interest rates in the stack.

Filling the gap between senior debt and your equity is where mezzanine debt comes into play. This layer is a powerful tool for investors looking to push their total leverage up to 80% or 85%. Because it sits behind the senior lender, mezzanine debt requires a specific legal framework known as an intercreditor agreement. This document is vital because it outlines the rights of each party during a default; it ensures the senior lender stays in control while giving the mezzanine lender a path to take over the equity if payments stop.

Senior Debt: Low risk, low cost, first priority.

Mezzanine Debt: Higher interest, secondary position, leverage booster.

LTV Targets: Aim for 65% senior debt to maintain a healthy debt service coverage ratio.

Senior debt is your cheapest capital, but mezzanine is your leverage accelerator. Use it wisely to bridge the gap without over-leveraging your asset's cash flow.

The Equity Layers: Preferred vs. Common

Preferred equity acts as the hybrid engine of the capital stack. It offers a fixed "pref" return, which currently ranges from 8% to 12% in most La Jolla syndications. This return acts as a hurdle; the preferred investors must receive their full percentage before the common equity holders see a single dollar of profit. It’s a favorite for high-net-worth individuals who want consistent passive income without the high-octane risk of the very top layer.

At the peak of the structure sits common equity. This is where the true wealth-building power of real estate lives. Common equity holders own the residual value of the property. When the asset appreciates by 25% over a five-year hold, this layer captures the lion's share of that growth. While it carries the highest risk of loss, it offers the highest potential for 2x or 3x equity multiples.

Within the common equity layer, roles are clearly defined to ensure professional execution:

General Partner (GP): The sponsor who finds the deal, manages the asset, and executes the business plan.

Limited Partner (LP): The passive investors who provide the bulk of the capital to fund the acquisition.

The Split: Profits are typically shared in a 70/30 or 80/20 split after the pref is met.

This synergy allows you to scale your portfolio and achieve professional mastery without being bogged down by the day-to-day operations of property management. By balancing these four layers, you create a resilient financial structure that can withstand market shifts while maximizing your personal upside.

Repayment Priority: Understanding the Waterfall and Risk

The waterfall is the heartbeat of any sophisticated real estate transaction. It dictates exactly how every dollar of profit flows through the capital stack. Think of it as a series of buckets. Cash flow from operations or a capital event, like a Q4 2023 sale, fills the top bucket first. Only after the senior debt is satisfied does the money trickle down to the mezzanine lenders, preferred equity, and finally, the common equity holders. In high-stakes La Jolla markets where entry prices often exceed $15 million, understanding this flow isn't just a technicality; it's the difference between scaling your wealth and losing your shirt.

Cash flow from monthly rents differs significantly from capital event distributions. During the hold period, operational cash flow focuses on debt service and preferred returns. However, a capital event like a 2024 refinance or a 5.2% cap rate sale triggers the "Last-In, First-Out" rule. This is the primary fear for every investor. If a deal underperforms and the asset value drops by 15%, the common equity is the first to be wiped out. The bank gets paid every cent before the equity holders see a dime. This makes the common equity holder the ultimate entrepreneur. You take the most risk, but you also unlock the highest rewards, often targeting an IRR north of 18%.

Order of Operations: Who Gets Paid When?

The sequence is absolute. First, the property pays its operating expenses, including taxes and insurance. Next comes the Senior Debt. These lenders have a first-priority lien. If the property generates $100,000 in Net Operating Income, and the mortgage is $60,000, the bank takes their cut before anyone else breathes. Subordination is the rule here. Every layer below the senior debt is "subordinate," meaning they have a lower claim on assets. If you're in a mezzanine position, you're essentially standing in line behind the bank. This hierarchy is enforced by strict covenants. For instance, a senior lender might require a Debt Service Coverage Ratio (DSCR) of 1.25. If the property's performance dips below that 1.25 mark, the bank can trap cash, preventing any distributions to the lower layers of the capital stack until the ratio improves.

Operating Expenses: Property management, repairs, and utilities.

Senior Debt: Fixed or floating rate bank loans.

Mezzanine/Preferred: Hybrid layers with fixed returns.

Common Equity: The GP and LP profit split.

Risk Mitigation Strategies for the GP

Smart General Partners don't just hope for success; they engineer it through conservative underwriting. You must stress-test your assumptions against a 100-basis-point interest rate hike or a 5% drop in occupancy. Use the Multifamily Analyzer to run these scenarios before you ever sign a Letter of Intent. This tool allows you to see exactly where the waterfall breaks under pressure. It's the best way to ensure your common equity position remains protected even if the market shifts.

Beyond the numbers, "The Network" is your most powerful defense. When a funding gap appears or a renovation budget increases by 12% due to material costs, having a direct line to seasoned operators and private capital partners is essential. Proximity to success provides the shortcut you need to solve capital problems fast. Don't go it alone. Leverage the collective intelligence of the community to dominate your local market and secure your path to passive wealth. Mastery of the stack ensures you aren't just playing the game; you're winning it.

Strategic Structuring: How to Optimize Your Stack for Maximum Leverage

Mastering the capital stack is the difference between owning a single asset and dominating a regional market. Your goal is to engineer a structure that minimizes your personal cash outlay while maximizing your internal rate of return (IRR). By layering debt and equity strategically, you can control a $50 million La Jolla complex with a fraction of the total cost. This isn't just about finding money; it's about financial engineering that accelerates your path to total lifestyle freedom. High leverage allows you to spread your capital across three deals instead of one, effectively tripling your wealth-building velocity.

Every layer you add changes your risk profile. High leverage, often reaching 80% to 90% of the total project cost, relies heavily on debt. This amplifies your gains during a market upswing but leaves less room for error if occupancy dips. Conversely, a heavy equity stack provides a safety net, lowering your break-even point by 15% or more. Successful investors use Preferred Equity to bridge the gap. This layer attracts investors with $5 million or more in liquid assets who prioritize capital preservation. You offer them a fixed 10% to 12% return, positioning them above common equity but below the senior lender. They get security; you get the capital needed to close the deal without giving up total control.

You must understand the cost of your capital to ensure the deal actually works. WACC is the heartbeat of your deal; if your asset return doesn’t beat this number, you don’t have a deal. To calculate this, you take the weighted average of the interest rates on your debt and the expected returns for your equity partners. If your WACC sits at 7.5% and the property only yields 6.8% in its current state, you are losing money every month. You must force appreciation through aggressive asset management to push that yield above your WACC as quickly as possible.

When to Go Deep: High Leverage Scenarios

In high-velocity Value-Add deals, pushing for 85% Loan-to-Cost (LTC) through mezzanine financing can explode your IRR from 15% to 25% or higher. This strategy works best on properties with a clear 18 to 24 month renovation cycle. You use expensive bridge debt to fund the turnaround, then execute a "Refinance and Exit" strategy. By June 2025, you could replace that 11% mezzanine loan with 6% permanent agency debt, effectively paying off the most expensive layers of your capital stack and locking in long term passive wealth.

Negotiating the Layers

Talking to a mezzanine lender requires a different script than pitching a private equity partner. Lenders want to see a 1.25x Debt Service Coverage Ratio (DSCR) and a bulletproof exit strategy. Private equity partners want to see your "skin in the game" and a clear path to a 2.0x equity multiple. To maintain control, ensure your operating agreement includes "drag-along" rights and specific buy-out clauses. Proximity to success is the ultimate shortcut. You can join the Multifamily Intelligence network to connect with the precise partners needed to fund your next La Jolla acquisition.

Mastering the Stack: From Theory to High-Stake Deal Execution

Mastering the capital stack serves as your primary engine for achieving total financial independence. It isn't just a technical diagram; it's the blueprint for the Multifamily Lifestyle. When you understand how to layer senior debt with mezzanine financing and private equity, you stop being a spectator in the real estate market. You become an architect of wealth. This level of mastery allows you to control $20 million assets in prime locations like La Jolla while minimizing your personal capital outlay. It's about leverage, scale, and the professional sophistication required to play in the big leagues.

Charles Dobens has spent decades deconstructing complex deal structures for investors who refuse to settle for mediocre returns. He has analyzed over 1,000 unique deal configurations, identifying the subtle pitfalls that can collapse a capital stack during a market shift. His expertise acts as the missing piece for investors who have the ambition but lack the structural roadmap. By connecting technical knowledge with aggressive execution, you move beyond the limitations of traditional financing and enter the world of high-velocity syndication.

The Multifamily Intelligence Advantage

The Personal Mentorship Program isn't a standard coaching course. It's a high-impact tactical environment designed to help you structure your first, or your next, complex deal with surgical precision. You'll gain direct access to the strategies needed to navigate the current 5.5% interest rate environment while still delivering 15% to 20% annualized returns to your investors. This program focuses on the practicalities of the "Multifamily Lifestyle," where freedom is bought through the mastery of asset management and deal flow.

Inside "The Network," you'll find a curated community of high-net-worth individuals and equity partners. These connections are vital when you need to fill the common and preferred equity layers of your stack quickly. Instead of cold-calling for capital, you lean on a community of peers who understand the value of a well-structured La Jolla deal. For those ready to transition from single-family units to 100-plus unit complexes, the 5-Day Multifamily Challenge provides the 100% clarity required to start this journey. It's the starting point for anyone serious about dominating the commercial space.

Next Steps: Stop Analyzing, Start Scaling

Analysis paralysis is the single biggest obstacle to building a legacy. Many investors spend 12 to 18 months "studying" the market while the best deals in Southern California are snatched up by those with the confidence to execute. Passive wealth isn't a dream; it's a mathematical certainty when you apply the right leverage to the right asset. You've learned the theory of the stack. You've seen how the layers protect your downside while uncapping your upside. Now, it's time to put that knowledge into motion.

The difference between a hobbyist and a professional investor is the willingness to seek mentorship and take decisive action. Don't let another quarter pass with your capital sitting on the sidelines. The market doesn't wait for the hesitant. The stack is ready. Are you?

Take Action Now: Apply for Personal Mentorship and Scale Your Portfolio Today

Scale Your Portfolio with a Precision-Engineered Stack

Mastering the capital stack isn't just a technical skill; it's the high-performance engine behind every successful multifamily acquisition. You've learned how to dissect the four core layers of a deal and how to structure the repayment waterfall to protect your equity. You now understand that optimizing leverage isn't about taking the most debt, but about balancing risk to accelerate your path to total lifestyle freedom. Theory only takes you so far in this fast-paced industry. To truly dominate, you need the tools and the network that bridge the gap between analysis and execution.

Founded by "The Multifamily Attorney" Charles Dobens, Multifamily Intelligence provides over 10 years of mentorship success to help you scale your portfolio with confidence. You'll gain exclusive access to proprietary deal analysis software that removes the guesswork from complex syndications and ensures your numbers are airtight. Stop watching from the sidelines while others close the deals you want. It's time to leverage the power of a proven blueprint and unlock the passive wealth you've been working for.

Your next legacy deal is within reach. Let's go build it.

Frequently Asked Questions

Is common equity the same as a down payment in a capital stack?

Common equity represents the 20% to 35% of the deal's total cost that investors fund directly. It's the foundation of your capital stack in La Jolla acquisitions. While it functions like a down payment, it sits at the bottom of the repayment priority list. You take the 100% loss risk first, but you also capture the unlimited upside once debt and preferred tiers are paid.

Can I change the capital stack after I have already purchased an apartment building?

You can absolutely restructure your financing after closing to unlock more Passive Wealth. Most 100-unit syndications in San Diego County target a 3-year to 5-year window for a supplemental loan or a full refinance. This move allows you to return 40% or more of the initial capital to your investors while keeping the asset. It’s a proven strategy to scale up your portfolio without selling.

How much mezzanine debt is too much for a multifamily deal?

Keep your mezzanine debt capped so the total loan-to-value (LTV) stays under 85%. Crossing this threshold creates a 20% higher probability of default during market contractions. High-performing operators in the 92037 zip code typically limit mezzanine layers to 10% or 15% of the total cost. This buffer protects your cash flow from being swallowed by double-digit interest rates during the 24-month stabilization phase.

What is the difference between preferred equity and a second mortgage?

Preferred equity is an ownership stake with a fixed 8% to 12% return, whereas a second mortgage is a recorded debt instrument against the title. Lenders often view a second mortgage as a breach of senior loan covenants. Preferred equity avoids this. It allows you to fill a 15% funding gap without the 30-day foreclosure risk associated with junior debt. Use it to dominate competitive bidding wars.

Does a higher capital stack always mean higher risk for the investor?

A taller, more complex structure doesn't automatically increase risk if your debt coverage ratio remains above 1.25. Risk is actually defined by the cost of capital and the 10% vacancy buffer in your underwriting. Adding a 5% sliver of preferred equity can actually lower your personal risk by reducing the amount of cash you have tied up in a single 50-unit property. Don't fear complexity; fear poor coverage.

How do I explain the capital stack to potential private equity partners?

Use a 4-tier visual diagram to show exactly how their 7% preferred return sits above common equity. Explain that the senior lender gets the first 65% of the value, while they occupy the next 10% to 20% slice. This transparency builds the trust needed to accelerate your deal flow. Show them the 18% internal rate of return (IRR) target to prove the structure works for their portfolio.

What happens to the capital stack if I decide to refinance the property?

Refinancing replaces the existing senior debt with a new loan, often at a 70% loan-to-value ratio based on the updated appraisal. This event triggers a capital event where you pay off any 12% mezzanine debt first. You then return the original 25% common equity to your partners. This maneuver shifts the capital stack toward a more stable, long-term debt profile that fuels your lifestyle freedom and professional mastery.

Is it possible to have a capital stack with only senior debt and common equity?

A two-tier structure is the standard for 75% of private multifamily acquisitions in the La Jolla market. You secure a 65% LTV senior loan and cover the remaining 35% with common equity from your network. This clean approach minimizes interest expenses and maximizes the monthly distributions for your partners. It's the most straightforward path to scaling up your assets without the friction of complex mezzanine terms.

Comments